In the rapidly evolving world of fintech, algorithmic lending, and high-frequency trading, it’s easy to get distracted by the “shiny new objects” of finance. However, whether you are a junior analyst at a local credit union or a senior VP at a global investment firm, the fundamentals of lending remain unchanged. At the heart of every successful lending decision lies a timeless framework: the 5 C’s of Credit.

If you are looking to build a resilient, high-growth career in banking, understanding these five pillars isn’t just a requirement—it’s your competitive advantage. In this guide, we’ll explore why the 5 C’s of Credit are the backbone of the industry and how you can master them to accelerate your professional journey.

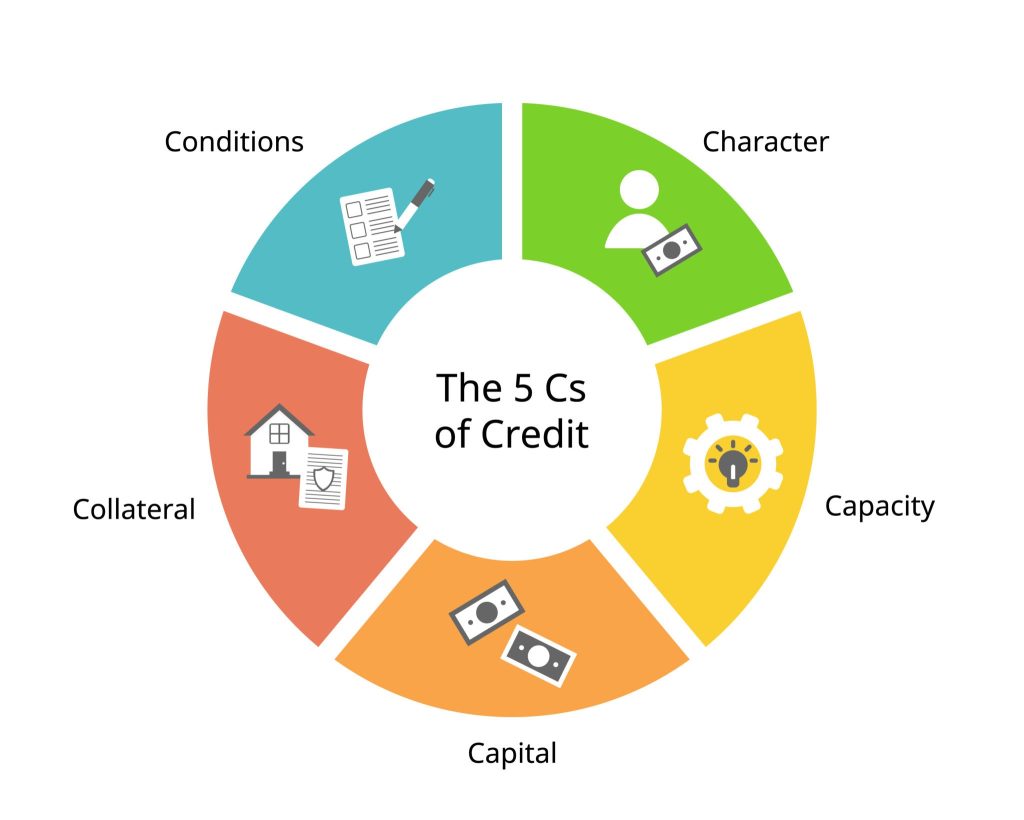

Understanding the 5 C’s of Credit

Before we dive into the career implications, let’s revisit the framework itself. The 5 C’s—Character, Capacity, Capital, Collateral, and Conditions—provide a holistic view of a borrower’s creditworthiness.

1. Character (The Human Element)

Character is often considered the most subjective yet critical “C.” It refers to a borrower’s reputation and track record. Does the borrower have a history of repaying debts on time? Do they exhibit honesty and integrity in their financial dealings? In a professional setting, credit analysts often look at credit scores and references to gauge this.

2. Capacity (The Ability to Pay)

Capacity measures the borrower’s ability to repay the loan using their primary source of income. For a business, this involves analyzing cash flow; for an individual, it’s about their debt-to-income ratio. This is where your skills from a financial analyst course become vital, as you learn to dissect income statements and determine if the numbers actually “pencil out.”

3. Capital (Skin in the Game)

Lenders are more comfortable when a borrower has a significant personal investment in a project. Capital represents the borrower’s own contribution. If a business owner is willing to risk their own savings, it signals confidence and provides a cushion for the lender.

4. Collateral (The Safety Net)

Collateral is an asset provided by the borrower to secure the loan. If the borrower defaults, the lender can seize the collateral to recover the loss. Understanding the valuation of assets—ranging from real estate to accounts receivable—is a core component of any comprehensive credit risk analyst course.

5. Conditions (The External Environment)

Finally, Conditions refer to the outside factors that could affect a borrower’s ability to repay. This includes the state of the economy, industry trends, and interest rates. A borrower might have great character and capacity, but if their industry is facing a massive downturn, the risk profile changes entirely.

Why the 5 C’s Matter for Your Career

You might wonder: “If I’m using advanced software to calculate risk, why do I need to know this manually?” The answer is simple: Judgment.

AI and machine learning can process data faster than any human, but they cannot always interpret the nuance of “Character” or the shifting “Conditions” of a niche market. By mastering the 5 C’s of Credit, you move from being a data entry clerk to a strategic decision-maker. This transition is exactly what separates a mid-level employee from an executive.

The Role of the Credit Risk Analyst

For those starting out, enrolling in a credit risk analyst course is the best way to see these 5 C’s in action. You’ll learn how to weight each “C” depending on the loan type. For example, in a secured mortgage, Collateral might carry more weight, whereas, in an unsecured personal loan, Character and Capacity are everything.

The Financial Analyst Perspective

If your goal is broader than lending, a financial analyst course will help you understand how these 5 C’s impact a company’s overall valuation. A company with poor “Capital” or a weak “Capacity” to service debt will see its stock price and credit rating suffer. Being able to spot these red flags early makes you an invaluable asset to any firm.

The Future of Credit: AI and Innovation

We are entering a new era of finance. We no longer rely solely on paper bank statements. Today, we use real-time data feeds and predictive analytics. To stay relevant, professionals are now looking toward a financial modeling with AI Course.

Incorporating AI into your workflow doesn’t replace the 5 C’s; it enhances them. AI can:

- Analyze Character: By scanning alternative data points that traditional credit bureaus might miss.

- Predict Capacity: Using machine learning to forecast future cash flows with higher accuracy.

- Monitor Conditions: By processing thousands of news articles and economic reports in seconds to flag changing market risks.

By combining the foundational knowledge of the 5 C’s of Credit with the technical prowess gained from a financial modelling with AI Course, you become a “hybrid professional”—someone who understands the “why” behind the numbers and the “how” of the technology.

How to Build Your “Credit Expert” Roadmap

If you want to make the 5 C’s the backbone of your banking career, follow these steps:

- Get Certified: Start with a specialized credit risk analyst course to understand the regulatory and technical side of lending.

- Master the Numbers: Take a financial analyst course to sharpen your ability to read balance sheets and income statements.

- Modernize Your Skills: Don’t get left behind by automation. A financial modelling with AI Course will teach you how to build the models that the banks of 2030 will be using.

- Practice Narrative Building: Every loan application is a story. Use the 5 C’s to tell the story of why a borrower is (or isn’t) a good bet.

Final Thoughts

The 5 C’s of Credit are more than just a mnemonic device from a textbook; they are the language of banking. They have survived economic depressions, industrial revolutions, and the rise of the internet. As you progress in your career, you will find that almost every complex financial problem can be boiled down to one of these five factors.

Invest in your education, master these fundamentals, and embrace the technological tools of the future. When you do, you won’t just be working in banking—you’ll be leading it.

No Comments